How to Use a Personal Loan to Build Credit

Building credit isn’t about magic tricks or “hacks.” It is about proving to lenders that you can borrow money and pay it back on time. One of the most effective tools for this is an installment loan.

When managed correctly, a personal loan adds positive data to your credit report every single month.

How a Loan Impacts Your Credit Score

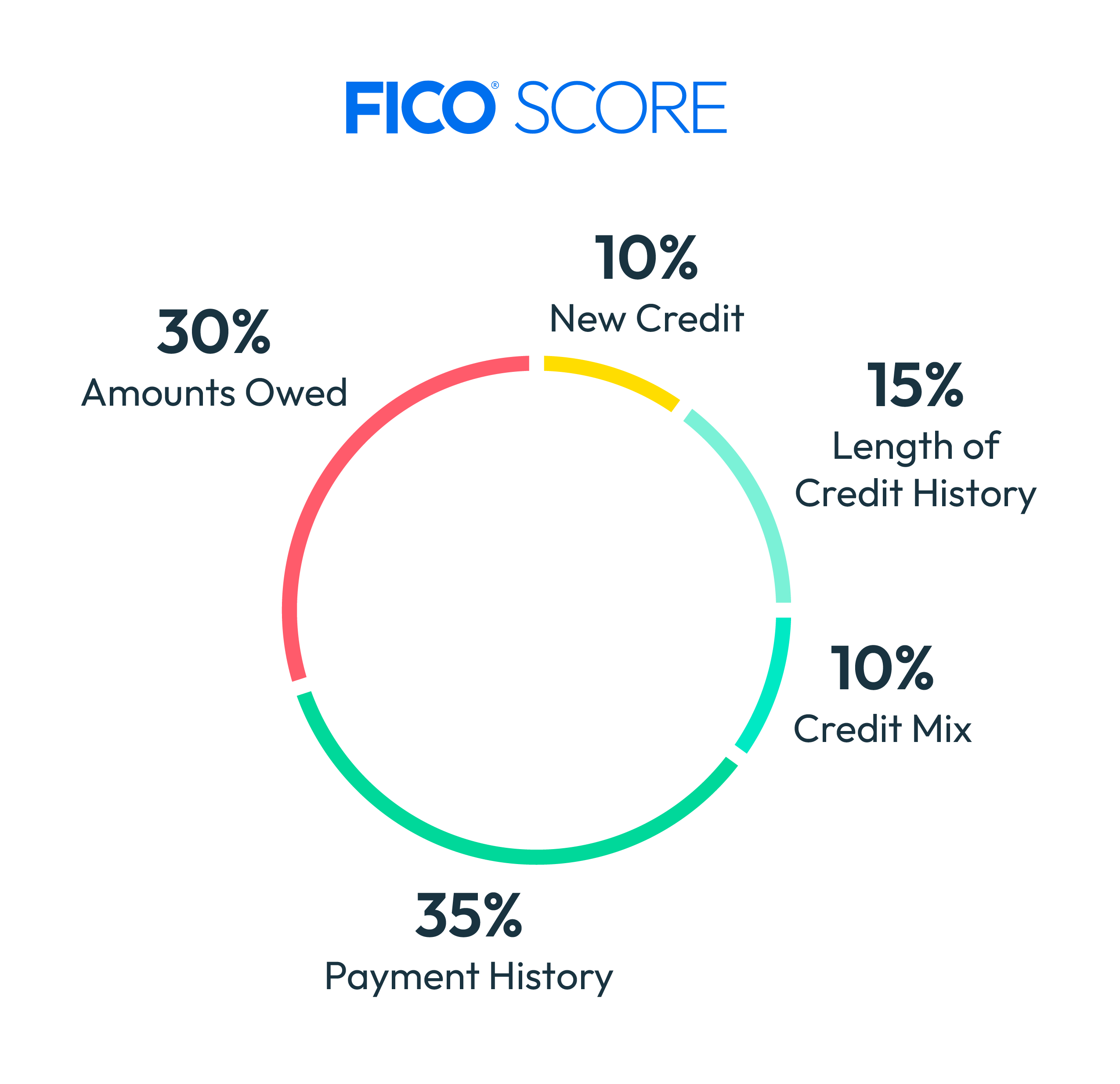

Your credit score is a numerical summary of your reliability as a borrower. According to FICO, the most widely used scoring model, your payment history makes up 35% of your score.

Taking out a loan helps your credit in three specific ways:

- Payment History: Every on-time payment is reported to the credit bureaus (Equifax, Experian, and TransUnion). A long streak of on-time payments is the single best way to raise a score.

- Credit Mix: Lenders like to see that you can handle different types of debt. If you only have credit cards (revolving credit), adding a personal loan (installment credit) improves your “credit mix,” which accounts for 10% of your score.

- Credit Utilization: If you use a personal loan to pay off high-balance credit cards, you lower your credit utilization ratio. This often results in a quick boost to your score.

The Difference Between Installment Loans and Revolving Credit

It is important to understand what kind of debt you are taking on. United Finance specializes in installment loans, which work differently than credit cards.

- Installment Loans (Personal Loans, Auto Loans): You borrow a specific amount of money and pay it back in equal monthly payments over a set period (the “term”). There is a clear start date and end date. This predictability makes it easier to budget.

- Revolving Credit (Credit Cards): You have a credit limit and can spend up to that amount repeatedly. The minimum payment changes based on your balance. It is easier to fall into debt spirals with revolving credit because there is no fixed end date.

Step-by-Step: Using a Loan to Build Credit

If your goal is to build or repair credit, you need a strategy. Don’t just borrow money without a plan.

1. Borrow Only What You Need

You do not need a massive loan to build credit. A small, manageable loan works just as well. The goal is to establish a track record of payments, not to burden yourself with debt.

2. Verify Reporting to Credit Bureaus

Not all lenders report to the major credit bureaus. Many “payday” lenders or online cash-advance apps do not report your on-time payments, meaning they do nothing to help your score. United Finance reports to credit bureaus, ensuring your good habits are recorded.

3. Set Up Autopay

Missing a payment by 30 days or more can significantly damage your credit score. The safest move is to set up automatic payments from your checking account to coincide with your payday. This removes the risk of human error.

4. Keep the Loan Open

Some borrowers try to pay off a loan as fast as possible to save on interest. While this saves money, keeping the loan open for at least six months to a year builds a longer history of on-time payments. A longer credit history is better for your score.

Common Mistakes to Avoid

Using debt to build credit requires discipline. Avoid these common errors:

- Applying for too many loans at once: Every formal loan application triggers a “hard inquiry” on your credit report. Too many inquiries in a short time can lower your score and make you look desperate for cash.

- Ignoring the APR: Always check the Annual Percentage Rate (APR) and total cost of borrowing. Ensure the cost of the loan is worth the benefit you are getting from it.

- Late payments: This defeats the purpose of the strategy. A single 30-day late payment can stay on your credit report for up to seven years.

The Value of Local Lenders

When you are building credit, you might hit a bump in the road. A changed job, a medical expense, or a scheduling error. Algorithm-based online lenders often have no flexibility. If you miss a payment, the computer marks it against you. Local community lenders, like United Finance branches in Oregon, Washington, and Nevada, operate differently. Because decisions are made by real people in your local branch (from Tacoma to Reno), you can often pick up the phone or walk in to discuss a solution before a missed payment hurts your credit report.