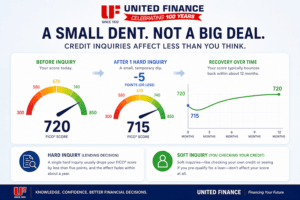

A single hard credit inquiry usually drops your FICO score by less than five points, and the effect fades within about a year. A soft inquiry, like checking your own credit or seeing if you pre-qualify for a loan doesn’t affect your score at all.

That’s the short answer. But there’s a real nuance worth understanding before you panic about applying for a loan, especially if you’re rate-shopping or rebuilding credit.

Soft Pull vs. Hard Pull: What’s the Difference?

A soft pull is essentially a background check. You trigger one when you check your own score in a credit app, when a lender pre-qualifies you, when you get a pre-approved credit card offer in the mail, or when an employer runs a background check.

A hard pull happens when you formally apply for credit. You’ve reviewed the terms, signed the application, and the lender is making a final lending decision based on your full credit file.

| Feature | Soft Inquiry | Hard Inquiry |

| Affects your score? | No | Yes (usually <5 points) |

| On your credit report? | Yes, but only you see it | Yes, visible to lenders for 2 years |

| Who triggers it? | You, lenders pre-qualifying, employers | You, by submitting a final application |

| Counted in scoring? | No | Yes, for ~12 months |

The Actual Damage: How Much Is “Less Than 5 Points”?

According to FICO, for most people, a single additional hard inquiry will take fewer than five points off their score. Some people see no measurable change at all. Others, particularly those with thin or short credit files, may see a slightly larger dip, sometimes closer to 10 points, because each data point carries more weight when there’s less history to balance it out.

Here’s what happens after the inquiry hits:

- It appears on your credit report immediately

- It stays on your report for two years

- FICO scoring models typically stop counting it after 12 months

- The impact fades gradually, not all at once

The trade-off math usually favors taking the hit. If a five-point ding lets you consolidate a maxed-out credit card with an installment loan, your score may actually rise — because credit utilization carries far more weight in your FICO score than inquiries do.

Rate Shopping: Multiple Inquiries Can Count as One

This is the rule most people don’t know about, and it matters a lot if you’re comparing loan offers.

FICO’s newer scoring models give you a 45-day window to shop for an auto loan, mortgage, or student loan. Multiple hard inquiries for the same type of loan within that window are counted as a single inquiry for scoring purposes. Older FICO models use a 14-day window. VantageScore uses a 14-day window across most loan types.

There’s also a buffer period: FICO ignores any mortgage, auto, or student loan inquiry made in the 30 days before scoring. So if you’re applying for a mortgage today, inquiries from the past 30 days don’t count against you yet.

What this means in practice: if you check rates with United Finance and one or two other lenders within two weeks, you’re not getting hit multiple times on your score. Shop confidently.

What Doesn’t Count as a Hard Inquiry

A lot of credit checks happen without affecting your score. None of the following are hard inquiries:

- Checking your own credit score (Credit Karma, your bank’s app, annualcreditreport.com)

- Pre-approved credit card offers you receive in the mail

- Insurance quotes (auto, home, life)

- Employer background checks

- Account reviews by lenders you already have credit with

A quick note on pre-approval vs. pre-qualification: the terms aren’t standardized across the industry. Pre-qualification almost always uses a soft pull. Pre-approval sometimes uses a soft pull and sometimes a hard pull, depending on the lender and product. Mortgage pre-approvals in particular often involve hard pulls. Always ask the lender directly which type of inquiry they’re running before you authorize it.

How Many Hard Inquiries Is Too Many?

There’s no official cutoff, but here are reasonable benchmarks:

- 1–2 inquiries in a year: Normal, no concern

- 3–5 inquiries in a year: Fine if spread across different needs (a car loan, a card, a refinance)

- 6+ in a short window: Lenders may read this as financial stress, especially if they’re all for the same type of credit outside a rate-shopping window

The bigger issue with stacked inquiries often isn’t the score points, it’s the pattern. A loan officer reviewing your file sees the inquiries directly and may interpret a flurry of recent applications as someone scrambling for credit, which can affect approval decisions independently of your score.

When You Should Actually Hold Off

Context dictates everything. Don’t apply for new credit if:

- You’re closing on a mortgage in the next 30–60 days. A hard inquiry right before funding can re-trigger underwriting and blow up the deal.

- You just submitted a major credit application. Stacking two big applications too close together makes lenders nervous.

- You’re borderline on a more important approval. If you’re 10 points below the cutoff for a better rate on something major, don’t burn those points on a non-essential application.

But if your transmission just scattered across I-5 and you need a car to keep your job? Take the five-point hit. Missing rent or losing income leaves a much deeper credit scar than any single inquiry.

What If There’s an Inquiry You Didn’t Authorize?

Pull your free reports at annualcreditreport.com and look for inquiries you don’t recognize. If you find one:

- Contact the lender listed on the inquiry — sometimes companies you’ve done business with appear under a parent company name you don’t recognize

- If it’s truly unauthorized, dispute it directly with the credit bureau reporting it (Experian, Equifax, or TransUnion)

- The bureau has 30 days to investigate and respond

- Consider placing a fraud alert or credit freeze if you suspect identity theft

The Consumer Financial Protection Bureau has detailed guidance on disputing inaccurate credit information at consumerfinance.gov.

How United Finance Approaches Your Application

Let’s be direct: yes, when you formally apply for a loan with United Finance, we run a hard credit pull. That’s how any lender making a real lending decision works. And as you’ve just read, the impact on your score is small and temporary, usually fewer than five points, mostly faded within a year.

What’s different about us is everything that happens around that credit pull.

A lot of lenders run your application through an automated system: hit their score threshold and you get an offer, miss it and you get a denial. There’s no conversation, no context, no human looking at your actual situation. We take the opposite approach. Before we make any decision, we can sit down with you, in person, at one of our branches across Oregon, Washington, Idaho, and Nevada, and we learn about you. What’s the loan for? What does your income and budget look like? What’s the story behind your credit history? You’re not a single number on a report.

A note on credit scores: We typically work best with borrowers who have a credit score of 600 or above. If you’re below that, it doesn’t automatically mean we can’t help, we look at the full picture, but a stronger score makes a meaningful difference in the rates and loan amounts we can offer. If you’re not sure where you stand, you can check your score for free at annualcreditreport.com or through your bank without affecting it.

The Short Version

- Soft pulls don’t affect your credit. Check your score and pre-qualify freely.

- A single hard pull costs fewer than 5 points and fades within a year.

- Rate shopping is protected. Multiple inquiries for the same loan type within 14–45 days count as one.

- Don’t apply right before a mortgage closes. Wait until the keys are in your hand.

- Fixing financial problems matters more than protecting 5 points. Consolidating debt usually moves your score up, not down.

Ready to See Your Options?

Checking your options with United Finance won’t affect your credit score. Find a local branch in Oregon, Washington, Idaho, or Nevada today.

Sources: FICO (myfico.com), Consumer Financial Protection Bureau (consumerfinance.gov), Experian (experian.com)